Severity: Notice

Message: Undefined variable: content_category

Filename: user/transcript.php

Line Number: 106

Severity: Warning

Message: Invalid argument supplied for foreach()

Filename: user/transcript.php

Line Number: 106

1) U.S. EQUITY RESEARCH Sector Watch December 21, 2015 Sam Stovall U.S. Equity Strategist HIKES & SPIKES Volatility Typically Picks Up After the Start of a Rate-Tightening Cycle Author of The Seven Rules of Wall Street S&P Capital IQ Global Markets Intelligence 55 Water Street New York, NY 10041 212-438-9549 sam.stovall@spcapitaliq.com A Hike in Rates In a classic case of “buy on rumor, sell on news,” the S&P Composite 1500’s 3% gain week-todate through December 16, was more than surrendered by the end of the week, causing the index to post a weekly decline of 0.4%, accompanied by Number of Days in Which the S&P 500 six of its sectors, and all three of its large-, mid- and Closed Higher/Lower by 1% or More small-cap components. In addition, 66% of its subindustries fell in price, led by declines of 7.0% or more 1%+ Daily Close Year Up Down Total for Diversified Chemicals, Diversified Metals & Mining, 2000 48 54 102 and Oil & Gas Storage & Transportation. The groups 2001 51 54 105 with the greatest gains were led by Aluminum, Coal & 2002 53 72 125 Consumable Fuels, and Water Utilities. 2003 45 37 82 And a Spike in Volatility In nearly two out of every three days this December, the S&P 500 rose or fell by 1% or more on a closing basis, versus an average of fewer than 30% of all trading days this year. Year to date through December 18, there have been 39 up days and 31 down days. During 2014, there were only 38 days of 1%+ up/down action, or nearly half the average annual volatility since 2000. Yet the rolling 12-month count rose steadily in 2015, starting at 38, hitting 50 by mid-year and at 71 now. 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Avg. 2000-15 21 13 16 31 59 62 39 48 29 21 19 39 37 20 17 13 34 75 55 37 48 21 17 19 31 38 41 30 29 65 134 117 76 96 50 38 38 70 75 Source: S&P Capital IQ. Past performance is no guarantee of future results. With More Likely to Come The threat of an increase in interest rates kept investors on edge since the start of the year. Only after combining the slowdown in the Chinese economy with the fear that the U.S economy was Tune in to “Stovall on Sectors” Every Friday on the S&P Capital IQ YouTube channel www.youtube.com/SPCapitalIQ Please follow me on Twitter: @StovallSPCapIQ S&P Capital IQ For more information 1-877-219-1247 This report is for information purposes and should not be considered a solicitation to buy or sell any security. Neither S&P Capital IQ nor any other party guarantees its accuracy or makes warranties regarding results from its usage. Redistribution is prohibited without written permission. Copyright © 2015 Standard & Poor’s Financial Services LLC, a part of McGraw Hill Financial, Inc. Redistribution, reproduction and/or photocopying in whole or in part is prohibited without written permission. All rights reserved. STANDARD & POOR’S, S&P, S&P 500, S&P EUROPE 350 and STARS are registered trademarks of Standard & Poor’s Financial Services LLC. S&P CAPITAL IQ is a trademark of Standard & Poor’s Financial Services LLC. Please see required disclosures on last 2 pages. 1

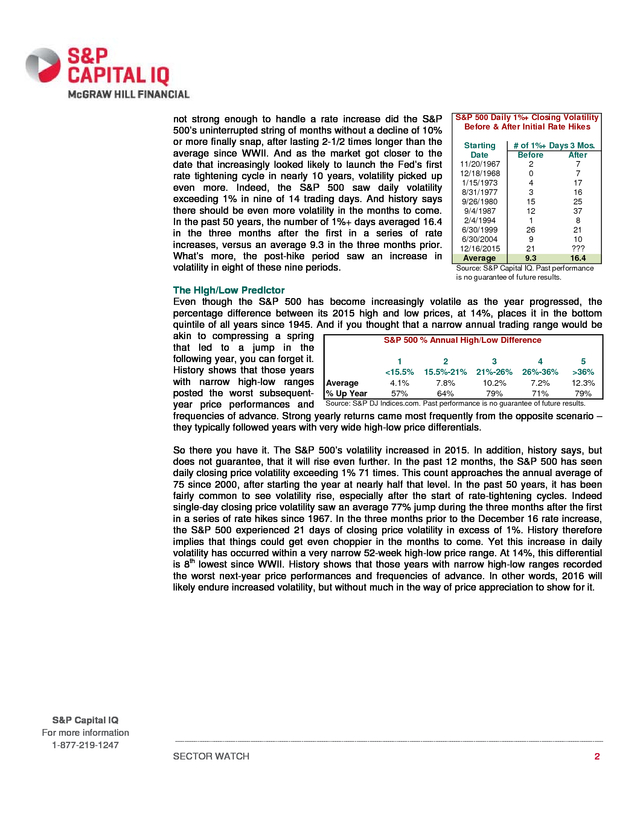

2) not strong enough to handle a rate increase did the S&P 500’s uninterrupted string of months without a decline of 10% or more finally snap, after lasting 2-1/2 times longer than the average since WWII. And as the market got closer to the date that increasingly looked likely to launch the Fed’s first rate tightening cycle in nearly 10 years, volatility picked up even more. Indeed, the S&P 500 saw daily volatility exceeding 1% in nine of 14 trading days. And history says there should be even more volatility in the months to come. In the past 50 years, the number of 1%+ days averaged 16.4 in the three months after the first in a series of rate increases, versus an average 9.3 in the three months prior. What’s more, the post-hike period saw an increase in volatility in eight of these nine periods. S&P 500 Daily 1%+ Closing Volatility Before & After Initial Rate Hikes Starting Date 11/20/1967 12/18/1968 1/15/1973 8/31/1977 9/26/1980 9/4/1987 2/4/1994 6/30/1999 6/30/2004 12/16/2015 Average # of 1%+ Days 3 Mos. Before After 2 7 0 7 4 17 3 16 15 25 12 37 1 8 26 21 9 10 21 ??? 9.3 16.4 Source: S&P Capital IQ. Past performance is no guarantee of future results. The High/Low Predictor Even though the S&P 500 has become increasingly volatile as the year progressed, the percentage difference between its 2015 high and low prices, at 14%, places it in the bottom quintile of all years since 1945. And if you thought that a narrow annual trading range would be akin to compressing a spring S&P 500 % Annual High/Low Difference that led to a jump in the following year, you can forget it. 1 2 3 4 5 History shows that those years <15.5% 15.5%-21% 21%-26% 26%-36% >36% with narrow high-low ranges Average 4.1% 7.8% 10.2% 7.2% 12.3% posted the worst subsequent- % Up Year 57% 64% 79% 71% 79% year price performances and Source: S&P DJ Indices.com. Past performance is no guarantee of future results. frequencies of advance. Strong yearly returns came most frequently from the opposite scenario – they typically followed years with very wide high-low price differentials. So there you have it. The S&P 500’s volatility increased in 2015. In addition, history says, but does not guarantee, that it will rise even further. In the past 12 months, the S&P 500 has seen daily closing price volatility exceeding 1% 71 times. This count approaches the annual average of 75 since 2000, after starting the year at nearly half that level. In the past 50 years, it has been fairly common to see volatility rise, especially after the start of rate-tightening cycles. Indeed single-day closing price volatility saw an average 77% jump during the three months after the first in a series of rate hikes since 1967. In the three months prior to the December 16 rate increase, the S&P 500 experienced 21 days of closing price volatility in excess of 1%. History therefore implies that things could get even choppier in the months to come. Yet this increase in daily volatility has occurred within a very narrow 52-week high-low price range. At 14%, this differential is 8th lowest since WWII. History shows that those years with narrow high-low ranges recorded the worst next-year price performances and frequencies of advance. In other words, 2016 will likely endure increased volatility, but without much in the way of price appreciation to show for it. S&P Capital IQ For more information 1-877-219-1247 SECTOR WATCH 2

3) Required Disclosures Glossary STARS Raking system and definition: ★★★★★ 5-STARS (Strong Buy): Total return is expected to outperform the total return of a relevant benchmark, by a wide margin over the coming 12 months, with shares rising in price on an absolute basis. ★★★★☆ 4-STARS (Buy): Total return is expected to outperform the total return of a relevant benchmark over the coming 12 months, with shares rising in price on an absolute basis. ★★★☆☆ 3-STARS (Hold): Total return is expected to closely approximate the total return of a relevant benchmark over the coming 12 months, with shares generally rising in price on an absolute basis. ★★☆☆☆ 2-STARS (Sell): Total return is expected to underperform the total return of a relevant benchmark over the coming 12 months, and the share price not anticipated to show a gain. ★☆☆☆☆ 1-STAR (Strong Sell): Total return is expected to underperform the total return of a relevant benchmark by a wide margin over the coming 12 months, with shares falling in price on an absolute basis. S&P Capital Ranking Definitions: Overweight rankings are assigned to approximately the top quartile of the asset class. Marketweight rankings are assigned to approximately the second and third quartiles of the asset class. Underweight rankings are assigned to approximately the bottom quartile of the asset class. S&P Capital IQ Quality Ranking Growth and stability of earnings and dividends are deemed key elements in establishing S&P Capital IQ's earnings and dividend rankings for common stocks, which are designed to capsulize the nature of this record in a single symbol. It should be noted, however, that the process also takes into consideration certain adjustments and modifications deemed desirable in establishing such rankings. The final score for each stock is measured against a scoring matrix determined by analysis of the scores of a large and representative sample of stocks. The range of scores in the array of this sample has been aligned with the following ladder of ranking. A+ Highest A High A- Above Average B+ Average B BC D Below Average Lower Lowest In Reorganization Required Disclosures Global Markets Intelligence (“GMI”) is a business unit of S&P Capital IQ. Standard & Poor’s Investment Advisory Services LLC (“SPIAS”) and McGraw-Hill Financial Research Europe Limited (“MHFRE”) (collectively, “GMI Investment Advisory Services” or “GMI IAS”), each a wholly owned subsidiary of McGraw Hill Financial, Inc., operate under the GMI brand. GMI IAS provides non-discretionary advisory services to institutional clients and does not provide advice to underlying clients of the firms to which it provides advisory services. In the United States, advisory S&P Capital IQ services are offered by SPIAS, which is authorized and regulated by the U.S. Securities and Exchange Commission. SPIAS does not act as a "fiduciary" or as an "investment manager", as defined under Employee Retirement Income Security Act (ERISA), to any investor. MHFRE, is authorized and regulated by the Financial Conduct Authority in the United Kingdom. Under the Markets in Financial Instruments Directive (‘MiFID’), MHFRE is entitled to exercise a passport right to provide cross border investment advice to European Economic Area (‘EEA’) States. MHFRE has duly notified the Financial Conduct Authority in the United Kingdom of its intention to provide cross border investment advice in EEA States in accordance with MiFID. MHFRE trades as S&P Capital IQ, does not provide services to “retail clients” and only has “professional clients” as defined under MiFID. In the United Kingdom to the extent the material is a financial promotion it is issued and approved by MHFRE. In Hong Kong, advisory services are offered by Standard & Poor's Investment Advisory Services (HK) Limited (“SPIAS HK”), which is regulated by the Hong Kong Securities and Futures Commission; in Singapore, by McGraw-Hill Financial Singapore Pte. Limited ("MHFSPL"), which is regulated by the Monetary Authority of Singapore; in Malaysia, by Standard & Poor's Malaysia Sdn Bhd (“S&P Malaysia”), which is regulated by the Securities Commission of Malaysia; and in Australia, by Standard & Poor's Information Services (Australia) Pty Ltd ("SPIS"), which is regulated by the Australian Securities & Investments Commission. In Korea, SPIAS holds a cross-border non-discretionary investment adviser license and it is registered with the Financial Supervisory Service (FSS). SPIAS, MHFRE, SPIAS HK, MHFSPL, S&P Malaysia and SPIS, each a wholly owned subsidiary of McGraw Hill Financial, Inc. operate under the GMI brand. GMI IAS offers four broad categories of investment advice: (i) portfolio strategies; (ii) fund research and recommendations; (iii) asset allocation; and (iv) analyses of certain U.S. and European fixed income securities using its proprietary Risk-to-Price scoring methodology. GMI IAS’ model portfolios (“model(s)”) are not collective investment funds. Assets managed in accordance with the models may lose money. GMI IAS is not responsible for client suitability and or the appropriateness of the service for the client. Any performance data quoted represents past performance. Past performance is not indicative of future returns. With respect to the investment recommendations made by GMI IAS, investors should realize that such investment recommendations are provided only as a general guideline. There is no agreement or understanding whatsoever that GMI IAS will provide individualized advice to any investor. GMI IAS is not responsible for client suitability. GMI IAS does not take into account any information about any investor or any investor’s assets when providing investment advice. GMI IAS does not have any discretionary authority or control with respect to purchasing or selling securities or making other investments. Individual investors should ultimately rely on their own judgment and/or the judgment of a financial advisor in making their investment decisions. Investments are subject to investment risks including the possible loss of the principal amount invested. An investment based upon GMI IAS’ investment advice should only be made after consulting with a financial advisor and with an understanding of the risks associated with any investment in securities, including, but not limited to, market risk, currency risk, interest rate risk and foreign investment risk. SPIAS, MHFRE and its affiliates (collectively, S&P) and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is 3

4) Required Disclosures provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Based on a universe of funds provided to SPIAS, SPIAS may include in a model portfolio or substitution list, if applicable, otherwise present as an investment option and/or recommend for investment certain funds to which S&P licenses certain intellectual property or otherwise has a financial interest, including exchange-traded funds whose investment objective is to substantially replicate the returns of a proprietary S&P Dow Jones Indices, such as the S&P 500. SPIAS includes these funds in models, otherwise presents them as an investment option and/or recommends them for investment based on asset allocation, sector representation, liquidity and other factors; however, SPIAS has a potential conflict of interest with respect to the inclusion of these funds. In cases where S&P is paid fees that are tied to the amount of assets that are invested in the fund or the volume of trading activity in the fund, investment in the fund will generally result in S&P receiving compensation in addition to the subscription fees or other compensation for services rendered by SPIAS. Poor’s Ratings Services may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at: www.standardandpoors.com/usratingsfees. GMI IAS may consider research and other information from affiliates in making its investment recommendations. The investment policies of certain model portfolios specifically state that among the information GMI IAS will consider in evaluating a security are the credit ratings assigned by Standard & Poor’s Ratings Services. GMI IAS does not consider the ratings assigned by other credit rating agencies. Credit rating criteria and scales may differ among credit rating agencies. Ratings assigned by other credit rating agencies may reflect more or less favorable opinions of creditworthiness than ratings assigned by Standard & Poor’s Ratings Services. For more detailed descriptions of disclosures and disclaimers such as investment risk and country conditions, please see: http://www.spcapitaliq.com/disclaimers/spias-investment-advisory-services Copyright © 2015 by Standard & Poor’s Financial Services, LLC. Redistribution, reproduction and/or photocopying in whole or in part is prohibited without written permission. All rights reserved. STANDARD & POOR’S, S&P and S&P 500 are registered trademarks of Standard & Poor’s Financial Services LLC. CAPITAL IQ is a registered trademark of Capital IQ, Inc. S&P CAPITAL IQ is a trademark of Standard & Poor’s Financial Services LLC. Standard & Poor’s Ratings Services does not contribute to or participate in the provision of investment advice and or model portfolios. Standard & S&P Capital IQ 4