1) Behavioral Finance

360°Behavioral View

May 2015

Our Periodic Review Exploring Multiple Topics Related to Behavioral Finance

• Market Driven • Economic • Psychological • Probabilistic • Investable •

Market Inflections…Sometimes the Tides Shift; Sometimes it is Just a Head Fake

The recent volatility in the price of oil has provided a good backdrop to review how

Sterling’s Behavioral Equity Strategies dynamically adjust to changing market

fundamentals and sentiment.

Oil Price Recap

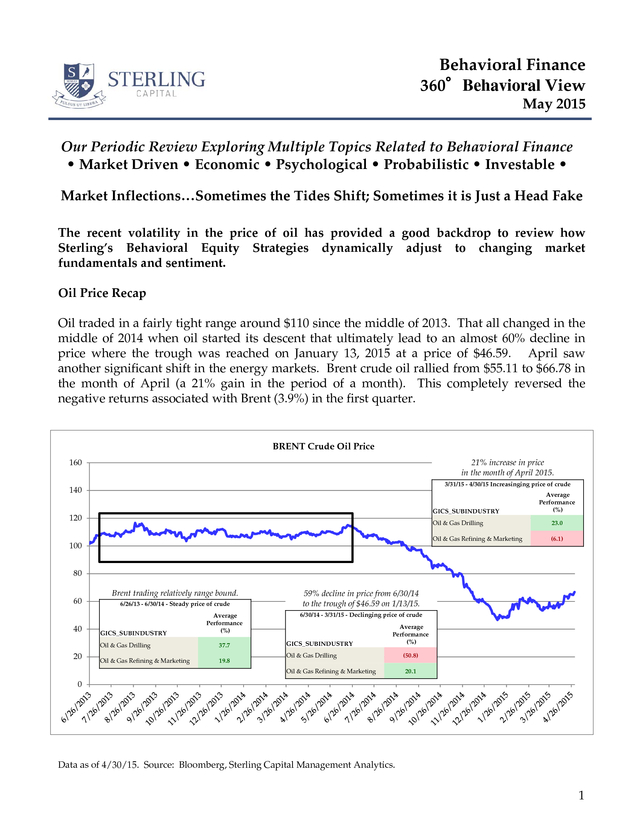

Oil traded in a fairly tight range around $110 since the middle of 2013. That all changed in the

middle of 2014 when oil started its descent that ultimately lead to an almost 60% decline in

price where the trough was reached on January 13, 2015 at a price of $46.59. April saw

another significant shift in the energy markets. Brent crude oil rallied from $55.11 to $66.78 in

the month of April (a 21% gain in the period of a month). This completely reversed the

negative returns associated with Brent (3.9%) in the first quarter.

BRENT Crude Oil Price

160

21% increase in price

in the month of April 2015.

3/31/15 - 4/30/15 Increasinging price of crude

140

GICS_SUBINDUSTRY

120

Average

Performance

(%)

Oil & Gas Drilling

Oil & Gas Refining & Marketing

100

23.0

(6.1)

80

60

40

Brent trading relatively range bound.

6/26/13 - 6/30/14 - Steady price of crude

GICS_SUBINDUSTRY

Average

Performance

(%)

Oil & Gas Drilling

20

37.7

Oil & Gas Refining & Marketing

19.8

59% decline in price from 6/30/14

to the trough of $46.59 on 1/13/15.

6/30/14 - 3/31/15 - Declinging price of crude

GICS_SUBINDUSTRY

Average

Performance

(%)

Oil & Gas Drilling

Oil & Gas Refining & Marketing

(50.8)

20.1

0

Data as of 4/30/15. Source: Bloomberg, Sterling Capital Management Analytics.

1

�

2) Behavioral Finance

360°Behavioral View

May 2015

Energy Sub Industry Analysis

Oil and gas drilling companies are heavily levered to the price of oil (they also have a fair

degree of financial leverage). At $110 a barrel, drilling can be quite lucrative. Indeed, from the

middle of 2013 through the middle of 2014 US large and midcap drillers’ average return was

over +37%. This contrasted with the refiners (less impacted by the price of oil) which had an

average return of just over +19% during the same period. As the price of oil fell significantly,

the drillers significantly underperformed the refiners; average returns of -50% relative to +20%

respectively. As the price of oil rebounded in April, those companies more highly levered to

the price of oil such as the drillers massively outperformed those less levered to the price of oil

as evidenced by the drillers average April 2015 return of +23% relative to the refiners of just

shy of -6%. During the rebound in price of oil we saw in April, the drillers significantly

outperformed the refiners as the prospect of higher oil prices on drillers earnings going

forward was viewed favorably by the market.

Sterling Capital Behavioral Portfolio Construction – A Dynamic Investment Process

Integral to our portfolio construction process is our stock ranking methodology that seeks to

capitalize upon investor biases and heuristics (rules of thumb). Each of our behaviorally

driven momentum and value factors is ranked relative to the entire investment universe (in the

case of large cap, the largest 1,000 stocks by market cap). The ultimate result leads to a

portfolio of stocks that is cheaper than and has more momentum than the associated

benchmark index. Sterling’s behavioral value and momentum ranks are dynamic: they adjust

as new information enters the market.

Behavioral Value and Momentum Ranks

(Lower is Better)

100

90

80

70

60

50

40

30

20

10

0

6/26/2013

9/30/2013

12/31/2013

3/31/2014

Oil & Gas Drilling

6/30/2014

9/30/2014

12/31/2014

3/31/2015

4/29/2015

Oil & Gas Refining & Marketing

Data as of 4/29/15. Source: Bloomberg, Sterling Capital Management Analytics.

2

�

3) Behavioral Finance

360°Behavioral View

May 2015

Using the previous two sub industries as an example, one can see ranks adjust as new information

comes to market.

Oil and Gas Refining and Marketing – A sub- industry that is less sensitive to absolute price of oil

US Large and Midcap refiners have exhibited favorable value and momentum traits to various degrees

from the middle of 2013 through today. What is interesting is that their ranks deteriorated at the

margin as the price of oil moved. In the time series ranks listed above one can see a noticeable decline

in rank between June and December 2014 in tandem with the fall in oil prices. This was largely driven

by momentum, specifically our behaviorally based Price Momentum coupled with Earnings Revisions

as analysts took into account the fact that refiners had a bunch of higher cost inventory (oil) on their

books that they would have refine and sell at lower prices. Once these adjustments were made, refiners

enjoyed a period of attractive relative returns as the costs of goods (oil) were aligned with their

proceeds (gasoline, other refined products).

Oil and Gas Drilling – A sub- industry that is more sensitive to absolute price of oil

This sub-industry is highly levered to the absolute price of oil (the higher the price, the more

profitable). Despite the average (hovering between the 50 and 60th percentile meaning average

behavioral value and momentum traits) constituent ranks of the sub-industry during the boom times,

there were companies in it that were attractive when the price of oil was trading around $110/barrel.

Once the oil price decline commenced, as can be expected, momentum collapsed led by earnings

revisions as analysts took down future earnings estimates which was followed by deterioration in price

momentum. Unlike the refiners, the momentum didn’t re-establish itself. This was due to the fact that

this subindustry is more sensitive to the absolute price of oil, at a price in the mid $40’s drilling for oil is

nowhere near as lucrative as $60 never mind $110.

BRENT Crude Oil Price

Rising oil prices:

Oil and Gas Drilling - Start to

outperform given prospects of

higher oil prices

Oil and Gas Refining and Marketing Start to underperform sub industries

with greater exposure to absolute

price of oil.

140

120

100

80

60

40

20

Range bound oil prices:

Oil and Gas Drilling - Favorable Price Momentum and Earnings Revision

possible given higher cost of oil.

Oil and Gas Refining and Marketing - Favorable Price Momentum and Earnings

Revisions possible given the range bound price of oil.

Declining oil prices:

Oil and Gas Drilling - Declining Earnings Revisions given profit margin squeeze.

Declining Price Momentum.

Oil and Gas Refining and Marketing - Declining Earnings Revision (temporary) given

higher cost inventory. Price Momentum declines but not as much as the Drillers.

0

Data as of 4/30/15. Source: Bloomberg.

3

�

4) Behavioral Finance

360°Behavioral View

May 2015

A Tale of Two Portfolios, or More Applicably a Portfolio in Transition:

Conclusion

More

Oil & Gas Drilling

% of

Energy

Exposure

8%

Oil & Gas Equipment & Services

15%

Oil & Gas Exploration & Production

15% 38%

Oil & Gas Storage & Transporta

Less

Sensitivity to Absolute

Price of Oil

6/30/2013

0%

Oil & Gas Refining & Marketing

45%

Integrated Oil & Gas

18%

Coal & Consumable Fuels

More

6/30/2014

0% 62%

% of

Energy

Exposure

Oil & Gas Drilling

12%

Oil & Gas Equipment & Services

24%

Oil & Gas Exploration & Production

5% 41%

Oil & Gas Storage & Transporta

Less

Sensitivity to Absolute

Price of Oil

As the price of oil collapsed, our behavioral

large cap value strategy dynamically shifted

energy exposure from a stance that was

positioned to capture the high price of oil to

one that was less susceptible to the price of

oil.

Below are three different periods

showing the energy exposure of a

Behavioral Large Cap Value representative

account. The first two cuts show how we

were positioned at peak oil, the last how the

portfolio had shifted exposure as the price of

oil declined. In the first two time periods,

notice how our overall exposure to subindustries that are more levered to the

absolute price of oil is little changed.

Contrast this with the 12/31/14 portfolio.

Note how the portfolio dynamically

adjusted to sub-industries less driven by the

absolute price of oil.

0%

Oil & Gas Refining & Marketing

41%

Integrated Oil & Gas

18%

Coal & Consumable Fuels

0% 59%

% of

Energy

Exposure

More

Less

Sensitivity to Absolute

Price of Oil

Our Behavioral based strategies are

specifically designed to trade on actual

12/31/2014

shifts in fundamentals and sentiment, not

Oil & Gas Drilling

4%

market “head fakes.” Over time more often

Oil & Gas Equipment & Services

12%

than not the market will go one direction in

Oil & Gas Exploration & Production

0% 16%

the short term only to turn on a dime and

Oil & Gas Storage & Transporta

22%

head the other direction. As the price of oil

continues to climb the odds are increasing

Oil & Gas Refining & Marketing

62%

that the portfolio will self-adjust and gain

Integrated Oil & Gas

0%

more exposure to those sub-industries that

Coal & Consumable Fuels

0% 84%

have greater exposure to the absolute level

Source: Sterling Capital Management Analytics

of oil as it becomes more attractive to own

them. That said it is futile to try to game the investment process. As of this time, our investment

process has not adjusted the portfolios due to this increase in oil price. One should be rest-assured, if

the trend persists (and or the price of oil doesn’t go back down and fundamentals support an

adjustment), much as we saw the adjustment occur on the way down to holdings less sensitive to the

price of oil, we will likely see the portfolio positions adjust and ultimately own more names that are

levered to the absolute price of oil.

FOR INSTITUTIONAL USE ONLY. NOT TO BE DISTRIBUTED OR COMMUNICATED TO THE GENERAL PUBLIC

The opinions contained in the preceding commentary reflect those of Sterling Capital Management LLC, and not those of BB&T Corporation or its executives. The stated opinions

are for general information only and are not meant to be predictions or an offer of individual or personalized investment advice. This information and these opinions are subject to

change without notice. Any type of investing involves risk and there are no guarantees. Sterling Capital Management LLC does not assume liability for any loss which may result

from the reliance by any person upon such information or opinions.

4

�